Front Page News:

The Effect of News Positioning on Financial Markets

Anastassia Fedyk

∗

March 12, 2018

Click Here for the Latest Version

Abstract

This paper estimates the effect of presentation of information on financial mar-

kets, using a natural experiment in prominent “front page” positioning of news on the

Bloomberg terminal. The front page and non-front page articles are indistinguishable

by either algorithmic analysis or by the target audience of active finance professionals.

Front page positioning induces 280% higher trading volumes and 180% larger price

changes within the first ten minutes after news publication, followed by a strong drift

for 30-45 minutes. Subsequently, non-front page news begins to catch up, but the

incorporation of this information is substantially more gradual, and the initial effects

of positioning persist for days after publication. The short-term effects induced by

positioning are even stronger than differences between articles of varying editorial im-

portance.

Keywords: information diffusion, news positioning, asset pricing, trading volume

∗

Harvard University, Department of Economics and Harvard Business School. Mail: Baker Library 244C,

25 Harvard Way, Boston, MA 02163. Email: [email protected]. I am particularly indebted to John Camp-

bell, Lauren Cohen, David Laibson, Chris Malloy, Andrei Shleifer, and Jeremy Stein for their invaluable

guidance and advice. I am also grateful to Daniel Andrei, Malcolm Baker, John Beshears, Joshua Coval,

Zhi Da (discussant), Kent Daniel, Stefano DellaVigna, Tatiana Fedyk, Xavier Gabaix, Tom Glocer, Robin

Greenwood, Sam Hanson, James Hodson, Marc Kaufmann, Patrick Kelly (discussant), Julien Penasse (dis-

cussant), Matthew Rabin, Stas Sokolinski, Adi Sunderam, Carmen Wang, Louis Yang (discussant), Vladimir

Zdorovtsov, Florian Zimmermann, and seminar participants at the Federal Reserve Board, Emory Univer-

sity, Georgetown University, Harvard University, Institut Jozef Stefan, London Business School, London

School of Economics, Stanford University, State Street Global Advisers, UC Berkeley, UCLA, University of

Virginia, University of Zurich, the American Finance Association, the European Finance Association, the

Trans-Atlantic Doctoral Conference, and the Western Finance Association for insightful comments. This

paper received the 2017 Best Ph.D. Paper Award from the European Finance Association and was a finalist

for the Hillcrest Behavioral Finance Award. I thank Lauren Cohen and Chris Malloy for sharing the Quant-

Quote data and Judes Echauz and Katelyn Haruki for providing outstanding research assistance. Funding

for this research was generously provided by the Harvard Business School, Hillcrest Asset Management, and

the Pershing Square Venture Fund for Research on the Foundations of Human Behavior.

1

1 Introduction

How does information get incorporated into asset prices? A number of theoretical models

propose potential frictions that may prevent even publicly available information from being

instantaneously reflected in prices.

1

Multiple empirical studies lend suggestive evidence to

this view.

2

However, tracing out incorporation of information in real time remains difficult,

and requires a detailed understanding of the variation across individual pieces of information.

In this paper, I capture the causal effect of presentation of news on the way the underlying

information is incorporated into asset pricing, using a natural experiment in the way news

articles are pinned to the top of the Bloomberg terminal news screen, in the “front page”

positions. I show that when the news is prominently positioned, the price response occurs

within an hour of publication. By contrast, for comparable non-front page news, the price

formation process takes 10-15 days to achieve the same response. In particular, within

ten minutes of publication, news articles that get pinned to the front page induce 280%

higher trading volumes and 180% larger price changes. Beyond that, front page articles

are accompanied by a strong price drift for approximately 30-45 minutes after publication,

consistent with the fact that these articles remain prominently positioned for approximately

half an hour. After that, the information in front page news appears to be fully incorporated,

and the reactions to non-front page articles begin to gradually catch up. However, the

incorporation of non-front page information is much slower: although the price paths after

front page and non-front page news eventually converge, this process takes multiple days.

Interestingly, differences in news positioning have an even stronger effect on short-term

market dynamics than differences between news articles marked with distinct importance

labels by the editorial staff.

My empirical design exploits a natural experiment based around a category of Bloomberg

news articles whose placement depends on the contemporaneous volume of other articles,

1

See, for example, Peng and Xiong (2006), DellaVigna and Pollet (2009), and Andrei and Hasler (2014)

on limited attention to publicly available information; and Harris and Raviv (1993), Kandel and Pear-

son (1995), Cao and Ou-Yang (2009), and Banerjee and Kremer (2010) on differential interpretations of

public information. A large related literature including Kyle (1985), Holden and Subrahmanyam (1992),

Wang (1994), Hirshleifer, Subrahmanyam, and Titman (1994), Cao, Coval, and Hirshleifer (2002), Foucault,

Hombert, and Ro¸su (2016), and Andrei and Cujean (2017), among others, considers incorporation of private

information.

2

See, for example, Foster, Olsen, and Shevlin (1984), Bernard and Thomas (1989), and Peress (2008) on

the post-earnings announcement drift; Bali, Peng, Shen, and Tang (2014) on inattention and underreaction

to liquidity shocks; Loh (2010), Da, Engelberg, and Gao (2011, 2015), Drake, Roulstone, and Thornock

(2012, 2015, 2016), Schmidt (2013), Curtis, Richardson, and Schmardebeck (2014), and Ben-Rephael, Da,

and Israelsen (2017) on predictability of market dynamics from proxies of attention; Huberman and Regev

(2001), Tetlock (2011), Gilbert, Kogan, Lochstoer, and Ozyildirim (2012), and Fedyk and Hodson (2015)

on reactions to stale news; and Carvalho, Klagge, and Moench (2011) and Marshall, Visaltanachoti, and

Cooper (2014) on reactions to false news.

2

rather than on their own content. I focus on news articles about individual U.S. equity

securities, and hand-collect a sample of news between March 2014 and December 2015. The

news articles in my hand-collected sample fall into three categories: “primary important,”

“secondary important,” and “all other” news. News articles marked as “primary important”

are always pinned to the prominent front page positions, displacing the previous front page

news and remaining on the front page for, on average, twenty to forty miutes. News articles

marked as “all other” are never placed into front page positions. News articles marked

as “secondary important” constitute the category of interesting variation. Any particular

news article in this category is given a front page slot if and only if, at the precise moment

when that article is released, there is at least one such slot remaining from the “primary

important” news. As a result, “secondary important” news articles that make it to the front

page and those that do not are marked as equally significant. Their positions vary due to

contemporaneous numbers of “primary important” articles, rather than their own underlying

content.

I structure the empirical analysis of the market dynamics following front page versus non-

front page “secondary important” news articles using a theoretical framework that reflects

standard models of limited attention and gradual information diffusion.

3

The three-period

model considers a news signal published by the main news source of interest and also reported

by alternative news sources. The framework incorporates two standard features from models

of gradual information diffusion: (1) only a fraction of investors are attentive to the news

signal from each source in each period; and (2) investors update their beliefs in a na¨ıve

Bayesian manner, incorporating their own information but not rational expectations of the

information available to other investors. Front page positioning is represented by more

prominent and longer-lasting reporting by the main news source. A larger incidence of

investors are attentive to the news signal from the main source when it is published on the

front page, and this persists into the second period.

This framework generates several predictions. First, the front page news articles are

accompanied by larger immediate trading volumes and absolute price changes. Second, the

initial returns accompanying front page news articles are more likely to continue in the

short-term. Third, the front page news articles induce lower longer-term price continuation.

My empirical results confirm these predictions. There are significant differences in market

dynamics following “secondary important” news articles that are pinned to the front page

and those that are not. Consistent with the first prediction, front page news articles are

accompanied by substantially higher trading volumes and absolute price changes for the

3

For models of limited attention and gradual information diffusion, see, for example, Hong and Stein

(1999), DellaVigna and Pollet (2009), and Andrei and Hasler (2014).

3

tagged securities immediately after publication. For example, these articles are, on average,

accompanied by 280% larger trading volumes and 180% larger absolute price changes during

the ten minutes following article publication.

Since pinning a news article to a front page position makes it visible for a longer period

of time, the front page positioning also induces more persistent short-term market reactions,

confirming the second prediction of the gradual information diffusion framework. Front page

news articles are accompanied by significantly higher serial correlation in price changes over

a variety of short-term horizons. For example, these articles are, on average, followed by

17% larger serial correlations in price changes across consecutive five-minute intervals.

I also find empirical support for the third prediction of the model: after the initial period

of about forty-five minutes, the price drift is significantly stronger for non-front page news

articles. Most front page articles are displaced from their prominent positions after twenty to

forty minutes, and the incorporation of front page information is virtually complete within an

hour of news publication. The incorporation of non-front page information takes much longer.

We begin to see some convergence during the first few hours after the news. For example,

the initial returns from the first 30-45 minutes after publication of non-front page news

are accompanied by a drift of 14-29% over the subsequent hour. However, the convergence

is quite gradual, and differences in price effects persist even days after news publication.

Securities mentioned in front page news articles see 34 basis points larger absolute cumulative

returns measured from the moment of publication to two days later, relative to securities

mentioned in non-front page news; this difference is statistically significant at the 10% level.

Five days out, the difference declines to a statistically insignificant 25 basis points, and

fifteen days after the news, the difference is a statistically indiscernible 8 basis points.

To contextualize the economic importance of these findings, I compare the market effects

of news positioning against the effects of news importance. In particular, I estimate market

dynamics following two sets of news articles that receive equally prominent positions but

that differ in their importance, as marked by the editorial staff. These are: (1) “secondary

important” articles that make it to the front page; and (2) “primary important” articles,

all of which make it to the front page by default. Articles in both of these categories are

prominently positioned, but the articles in the second category are marked by the editorial

staff, ex ante, to be more important than those in the first category.

I find that news importance is not as significant in driving short-term market activity

as positioning. Trading volumes induced by news publication are not statistically different

for securities mentioned in more (“primary important”) versus less important (“secondary

important”) news articles pinned to the front page. Absolute price changes are 80% (66%)

larger during the first five (ten) minutes following the more important news articles, but

4

the relative difference is smaller than that induced by the news positioning. The short term

price drift is statistically indistinguishable for more and less important news articles, holding

front page position constant. Overall, the results indicate that news positioning plays an

even larger role for short-term market dynamics than editorial markings of the importance

of the underlying news.

I perform a number of additional analyses to confirm that the results are not driven

by systematic differences between “secondary important” articles that receive a front page

slot and those that do not. First, I consider the possibility that, due to market participants’

distraction during periods with high volumes of news, articles published during quieter times

garner larger reactions. To address this possibility, I hold position constant and compare non-

front page “secondary important” articles released during times with different amounts of

contemporaneous news activity. I document that the non-front page articles released during

quiet times are, if anything, accompanied by less substantial reactions than the non-front

page articles released during busy times.

Second, using techniques from machine learning and a representative corpus of financial

news from Reuters, I learn the mixtures of topics generally discussed in financial news, such

as earnings announcements, technology, and litigation. I then use the trained model to com-

pare the distributions of identified topics appearing in the text of the individual Bloomberg

news articles in my hand-collected samples. I find no systematic differences between the dis-

tributions of topics discussed in the front page versus non-front page “secondary important”

news articles. The distribution of topics covered by the “primary important” news articles,

by comparison, does differ slightly from the distribution of topics appearing in “secondary

important” news.

Third, a survey of 150 active finance professionals indicates that absent salient posi-

tioning, market participants find front page “secondary important” headlines to be indis-

tinguishable from the non-front page ones. The survey participants consist of key decision

makers at a broad range of financial institutions, including broker dealers such as Bank of

America and Goldman Sachs, investment management firms such as BlackRock and PIMCO,

hedge funds such a Bridgewater and AQR, and private equity firms such as Blackstone and

Warburg Pincus. The finance professionals confirm Bloomberg editorial staff’s judgment of

news importance. They consistently identify the “primary important” news articles as, on

average, more impactful than “secondary important” news articles (“primary important”

headlines are chosen as more impactful 61% of the time, significantly different from 50%).

By contrast, these finance professionals identify the front page “secondary important” news

articles as more impactful than their non-front page counterparts only 48% of the time, not

significantly different from 50%. I also repeat this analysis using a smaller survey of 27 MBA

5

students from top business schools and find qualitatively similar results.

My findings build on the growing literature evaluating the impact of media on financial

markets.

4

Prior empirical strategies for estimating the causal impact of media use exoge-

nous variation in news arrival through weather-related disruptions (see Engelberg and Par-

sons (2011)), newspaper strikes (see Peress (2014)), disruptions to boat routes (see Koudijs

(2016)), and staggered implementation of robo-journalism (see Blankespoor, deHaan, and

Zhu (2017)), as well as variation in security relevance tags (see von Beschwitz, Keim, and

Massa (2017)) and headline complexity and degree of quantification (see Umar (2017) and

Huang, Nekrasov, and Teoh (2017)). Klibanoff, Lamont, and Wizman (1998) find that for

closed-end country funds, the incidence of news on the front page of the New York Times is

correlated with a higher elasticity of price with respect to asset value. Huberman and Regev

(2001) further highlight the importance of prominent news positioning by analyzing a case of

(mostly) stale information, initially reported in Nature in November 1997, getting reprinted

on the front page of the New York Times in May 1998. Furthermore, Lawrence, Ryans, Sun,

and Laptev (2017) present compelling evidence that promotion of earnings announcement

news on Yahoo! Finance to a subset of website visitors increases the abnormal return on the

announcement date.

5

The present paper contributes to the literature by providing a clear counterfactual. The

natural experiment in positioning of news on the Bloomberg terminal offers clean variation

in institutional investor attention in an important setting that represents the main source of

information for a large set of finance professionals. This allows me to document two things.

On the one hand, when information is especially saliently highlighted, the market response

is quite efficient: prices respond within an hour (and largely within the first minutes) of

news publication. These highlighted news events, for which limited attention and cognitive

processing limitations play a minor role, illustrate a best-case scenario. On the other hand,

the price formation process is this efficient only for especially highlighted news. In other cases

– even with public, easily accessible news consumed by sophisticated institutional investors

– attention is more gradual and the price formation process takes substantially longer, on

the order of days or even weeks.

4

See Busse and Green (2002), Barber and Loeffler (1993), Chan (2003), Fehle, Tsyplakov, and Zdorovtsov

(2005), Antweiler and Frank (2006), Barber and Odean (2008), Fang and Peress (2009), Engelberg, Sasseville,

and Williams (2012), Solomon (2012), Dougal, Engelberg, Garc´ıa, and Parsons (2012), Rogers, Skinner, and

Zechman (2013), Hillert, Jacobs, and M¨uller (2014), Ahern and Sosyura (2014), Liu, Sherman, and Zhang

(2014), Yuan (2015), and Boulland, Degeorge, and Ginglinger (2017).

5

The importance of prominent positioning and alphabetical ordering has also been documented in other

contexts; see, for example, Ho and Imai (2008), Jacobs and Hillert (2015), and Feenberg, Ganguli, Gaule,

and Gruber (2017). In financial markets, presentation has been shown to drive mutual fund flows (Kaniel

and Parham (2017)) and attract attention to securities independent of information flows (Wang (2017)).

6

These findings provide systematic evidence that it is not enough to make financially-

relevant information easily accessible: how saliently the information is presented plays an

important role in determining whether the information is immediately reflected in asset

prices. The price impact induced by front page positioning occurs quickly, but the compa-

rable non-front page information takes surprisingly long to converge, given that these are

all easily accessible news articles available on the Bloomberg terminal. For more obscure or

private information, similar mechanisms are likely to apply at longer horizons, generating

phenomena such as months-level momentum.

The remainder of the paper proceeds as follows. Section 2 describes the data and the

natural experiment in news positioning. Section 3 outlines the conceptual framework of

market dynamics following more and less prominently positioned news. Section 4 presents

the key empirical findings on the differential market dynamics following front page and non-

front page news articles. Section 5 explores the effect of news importance, holding position

constant, by comparing “secondary important” news articles that are positioned on the front

page against “primary important” front page news articles. Section 6 presents additional

analyses of news content, confirming that the front page “secondary important” articles in

the sample are indistinguishable from their non-front page counterparts by both algorithmic

analysis and the target audience of market participants. Section 7 concludes.

2 Data Sources and Empirical Strategy

In order to capture the casual effect of news presentation on trading volumes and returns,

I use quasi-random variation in positioning of news articles on the Bloomberg terminal.

Two key features of these data make them especially well-suited to the current analysis.

First, Bloomberg is one of the largest financial news providers and a main source of news

for finance professionals, making it an ideal setting to estimate the effect of attention to

news on financial markets. Second, the data include a natural experiment of quasi-random

positioning for a subset of news articles. The news data are merged with market data to

relate news presentation to trading volumes and price formation.

2.1 Natural Experiment in News Positioning

In this subsection, I describe the quasi-random variation in news positioning that I use

in my research design. In particular, I concentrate on a subset of news articles that are

sometimes prominently positioned, and sometimes not, depending on the volume of other

articles released around the same time and not on the characteristics of the news articles

7

themselves.

The full sample of news passing through the Bloomberg terminal is aggregated from a

variety of sources in real-time. The sources of news include key national and international

news wires from a comprehensive set of news organizations, company filings, press releases,

and content from web sources, including blogs and social media. The news articles are

disseminated electronically to over 300,000 finance professionals through the subscription-

based terminal. Overall, there are millions of articles tagged with U.S. equity securities

during the sample period of March 22, 2014 - December 31, 2015.

There are differences in how Bloomberg presents individual news articles on the terminal.

Generally, the news screen features a scrolling list of news articles, where newly published

articles replace the older ones at the top of the screen. However, some of the news articles

written directly by Bloomberg News get pinned to the top of the screen. At any given point

in time, there are at most three such pinned articles. Figure 1 shows a screenshot of a

default Bloomberg news screen covering all company-relevant news. The top three articles

are pinned and remain at the top, while the articles below continually move down as new

publications arrive. It is these positions, highlighted in yellow font at the top of the default

company news screen in Figure 1, that I term “front page” throughout this paper.

Effectively, there are three broad categories of news articles passing through the Bloomberg

terminal: the primary “primary important” (PI) articles; the “secondary important” (SI)

articles, and “all other” articles. The assignment of individual articles to these categories

reflects the journalistic and editorial opinion regarding the importance of a given piece of

news. Each of the two important categories, PI and SI, comprises roughly 0.1-0.5% of all

news, so both of these categories of articles capture news of fairly rare perceived importance.

I exclude market wrap articles, in order to focus on new information relevant to individual

securities, and hand-collect all articles that are tagged with at least one publicly traded U.S.

equity security, that are published between 8AM and 5PM EST during the sample period,

and that are either in the PI category (1,419 unique PI articles) or the SI category (4,887

unique SI articles).

For the most part, PI articles represent significant company news, such as earnings reports

and M&A decisions. A few representative examples of the sample of PI news are provided

in Panel 1 of Table 1.

SI articles likewise include significant events, such as changes in regulation and drug

approvals. However, this set of news also features articles that are likely to capture the

readers’ curiosity, but that are less immediately relevant to financial markets, such as moves

of top well-known traders and perks in financial firms. A few representative examples of SI

articles are presented in Panel 2 of Table 1.

8

The classification of articles into categories of relative importance plays a role in how

prominently the articles are positioned. When an article from the PI category is released, it

is immediately placed in a prominent front page position, displacing whichever news article

was in that position previously. Once on the front page, a news article remains there until

the earlier of two things occurs: either a new PI article comes out and displaces the old

article, or a predefined amount of time (on the order of hours) elapses. Occasionally, there

are not enough PI articles at a given point in time to fill all of the front page slots. In this

case, the next SI article to be published, upon its release, takes the available front page

position. The process of article positioning is depicted in Figure 2.

As a result, there are two categories of news articles deemed equally important but having

different positions: the SI articles that come out at a time when there are available front

page slots and the SI articles that come out at a time when front page slots are unavailable.

I hand-collect the positions of the SI articles in my sample. This subset of the news sample

– SI articles in various positions – forms the basis for my causal analysis.

Screening of the articles confirms that there are no systematic differences in content

between SI news articles that are placed on the front page and those that are not. Both

include significant events, such as:

• “T-Mobile Said to Plan to Turn Down Iliad’s $15 Billion Offer” (not front page)

• “Chipotle Probed for New Outbreak of Different E. Coli Strain” (front page)

But both front page and non-front page SI news articles also feature news events that

carry less immediately relevant impact for financial markets. For example:

• “Morgan Stanley Gets 90,000 Applications for Summer Program” (not front page)

• “Pimco Said to Have Discussed Firing Gross Before Exit to Janus” (front page)

In Section 6.2, I compare the texts of the front page and non-front page SI news articles

formally using machine learning techniques. I find no systematic differences between the

two categories of news. Similarly, a survey of active finance professionals and MBA students

from top business school programs indicates that human financial experts do not perceive the

front page SI news articles to be any more significant than their non-front page counterparts.

Table 2 presents the distribution over time of PI and SI news articles published between

the hours of 8AM and 5PM. All numbers are cited in ticker-articles, so that articles tagged

with more than one U.S. equity security ticker are included one time for each tagged U.S.

security. Overall, there are 2,362 PI article-tickers in the sample and 8,233 SI article-tickers,

of which 1,274 are given a front page position. The articles are roughly evenly distributed

9

across the months of the year, with a lower volume of articles in January and February (and,

to a lesser extent, March), since the sample begins on March 22, 2014 and hence does not

cover these months in 2014. Over hours of the day, PI news articles peak at the start and end

of the business day, during 8-10AM and especially during 4-5PM, while the SI news articles

are more evenly distributed during the day. Consistent with the SI articles’ positioning being

determined by the concurrent volume of PI news, a lower percentage of SI articles makes it

to the front page during the hours that see a higher volume of PI articles. The correlation

between the hourly numbers of PI articles and the hourly likelihoods of SI articles receiving

front page positions is -81%.

Examining the timing of news releases in the sample, I find no evidence of strategic

release timing of the SI news articles. Of all the front page SI news articles, only 1.4% have

a non-front page article released up to one minute before or after the front page article’s

publication. Similarly, only 0.7% of the front page SI articles are accompanied by non-front

page SI articles within 30 seconds before or after. A mere 0.2% of the articles in the front

page SI sample have a non-front page article released within 10 seconds of their publication.

This low volume of SI news articles leaves little scope for influencing article position by

strategically timing the exact seconds of when the articles are released. As a result, the

process is unlikely to be contaminated by editorial staff being faced with multiple SI articles

to be released at the same time and strategically releasing the more important ones first.

I also find that the article volume does not appear to be driven by editorial targets. I

observe the distribution of articles across days and find that the volumes of PI and SI news

articles vary dramatically from day to day. The number of PI news articles ranges from 0 to

40 per day, while SI articles can number anywhere between 0 and 67 per day. There is also

little relationship between the numbers of PI and SI articles on any given day. The daily

numbers of the two types of articles display a low correlation of 25%. As shown in Figure 3,

any given day can see a large number of PI articles accompanied by few SI articles, and vice

versa. Overall, the distribution of PI and SI articles across days indicates that the editorial

staff is not targeting particular numbers of high-importance articles. Instead, the patterns

are more consistent with the evaluation of each article’s importance being based on its own

merit, independently of the volume of other news.

2.2 Market Data

I use the security ticker tags to merge the news position data with market data from

several sources. Industry classification, market capitalization, and shares outstanding come

from Compustat. High frequency price and trading data come from QuantQuote. The

10

second-resolution QuantQuote data include all tickers listed on NYSE and NASDAQ ex-

changes, and provide prices and numbers of shares traded for each second during the market

open. The data are adjusted for splits, dividends, and symbol changes.

The high frequency tests are run using news articles tagged with all firms for which

there are pricing data in QuantQuote, and shares outstanding and NAICS industry codes in

Compustat. The merged sample includes 948 front page SI article-ticker pairs, 4,930 non-

front page SI article-ticker pairs, and 1,650 PI article-ticker pairs. All of these article-ticker

pairs have at least one price data point in QuantQuote on the day of publication, but not

necessarily within shorter windows. Recall that PI news articles are more likely to come out

during the hours of 8-9AM EST and especially 4-5PM EST. As a result, the empirical tests,

which require market data within short windows of publication, reduce the PI news sample

more substantially than the two SI news samples.

3 Conceptual Framework

In this section, I present a conceptual framework formalizing the intuition regarding the

differences between front page and non-front page news articles. I outline two key aspects in

the way investors are likely to pay differential attention to news articles in different positions,

and then trace out the implications of these aspects for the process of incorporation of

information into asset prices.

The conceptual framework follows the setups in Hirshleifer and Teoh (2003) and Della-

Vigna and Pollet (2009). There is a risk-free asset with a zero rate of return and a single

risky security with a stochastic payoff R normally distributed with mean R and variance σ

2

R

,

realized in an unmodeled final period T . In the relatively short-term empirical settings that

I consider, the realized value R can be taken to denote, for example, the price on which an

asset settles in the days following an earnings announcement or the price of the combined

enterprise following an acquisition. The risky asset is in fixed supply X. For expositional

simplicity, I fix X = 0, so that the asset is in zero net supply; this simplifies the notation

without affecting the results.

There is a continuum of investors with total mass equal to 1, who maximize mean-variance

utility. In particular, let W

(i)

denote investor i’s final wealth at the end of the game at time

T . Then at any point in time t, investor i maximizes expected utility of the form

E

i,t

{W

(i)

} −

A

(i)

2

V ar

i,t

{W

(i)

} (1)

with respect to his current holdings. For expositional simplicity, I take the risk-aversion

11

coefficient to be identical across investors and normalize it to one: ∀i, A

(i)

= 1. Each

investor i is initially endowed with wealth W

(i)

0

. There are no liquidity constraints.

Information in this framework is modeled as a signal arriving at a particular point in

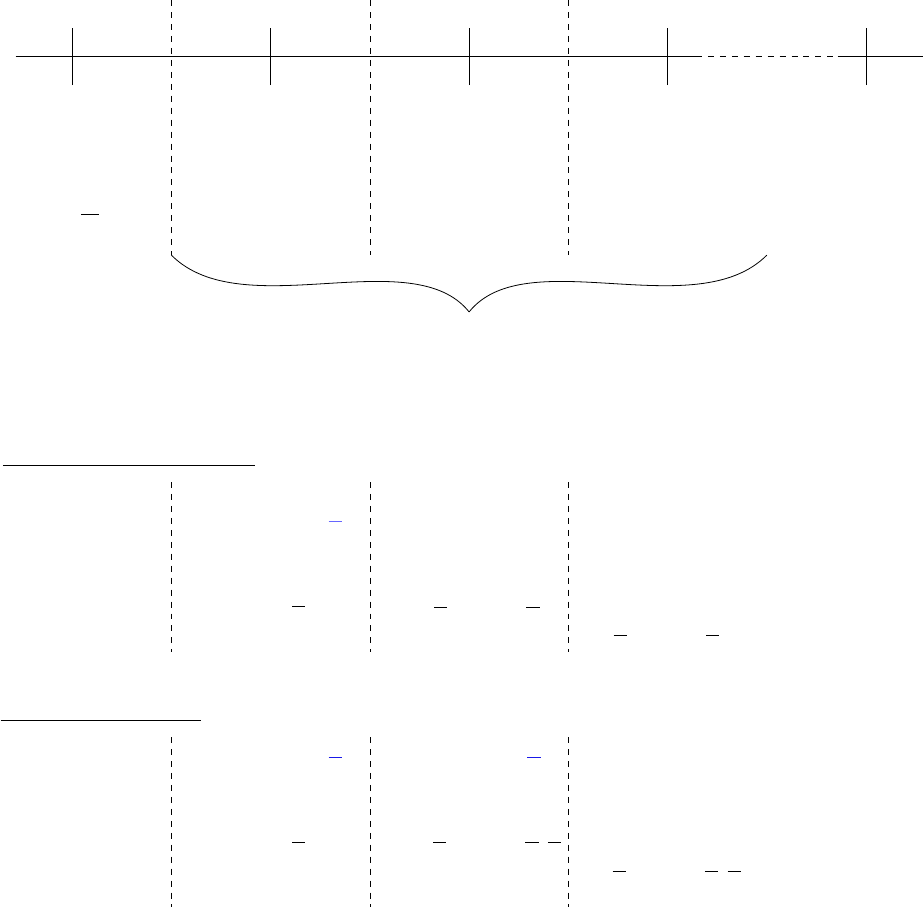

time and gradually diffusing across the population of investors. In particular, there are four

periods in the model. In period 0, investors form prior expectations regarding the distribution

of R. In period 1, a noisy signal (news) is released, and investors update their expectations

accordingly. In periods 2 and 3, investors continue to update their beliefs following the news

signal. At the end of the game, in the unmodeled period T , the true value of R is realized

and the investors consume their final wealth. I assume the following form for the news signal:

N = R + , where is a normally distributed noise term, independent of R, with mean 0

and variance σ

2

.

The news signal is not immediately observed by all investors. Instead, the main news

source, S, reports the news signal N for some number of periods. Mass γ > 0 of investors

are attentive to the main source S in each period t. Thus, in each period t that S reports

the news signal N, a fraction γ of investors who had not observed the news signal prior to t

now become aware of N.

I model the difference between front page and non-front page news with two key features.

First, front page news articles induce more attention overall, so that the fraction of investors

attentive to the news signal is higher: γ = γ in the case of front page news and γ = γ < γ

in the case of non-front page news. Second, front page new corresponds to the signal being

reported by S for longer. Thus, for non-front page news, investors can observe the signal N

from the main source S only in period 1. For front page news, by contrast, investors can

also observe the signal from the main source S in period 2.

Investors may also learn the news from alternative sources, albeit at a lower rate. In

particular, in any period when the news is not being reported by S, a fraction ξ > 0 of

uninformed investors still observe the news signal. This additional information channel can

be interpreted as investors finding the news through filters or active searches once it scrolls

off the top of the Bloomberg terminal screen, or reading the news from other providers. This

channel is a minor one in the model, and I assume that most investors who receive the news

do so from the main source S. In particular, I assume that:

ξ <

1 − γ

1 − γ

γ (2)

This condition ensures that once the main news source stops actively reporting the news

(i.e., when the news is not on the front page), the fraction of informed investors does not

increase faster than when the source continues to report (front page news). Consistent with

12

the information disseminating relatively slowly over the short horizons considered in my

empirical analysis, I also assume that both γ and ξ are small: γ, ξ << 1/2.

The model timeline is depicted in Figure 4. In each period t, let I

t

denote the set of

informed investors, who observe the news signal either during or prior to t, and let F

t

= |I

t

|

be the share of informed investors. I denote the remaining uninformed investors by U

t

. Let

F

F P

t

and F

NF P

t

denote the values of F

t

in the cases of front page and non-front page news,

respectively. Figure 4 illustrates the arrival of information and the evolution of the share of

informed investors for both front page and non-front page news.

The key frictions in the model are that (1) some investors are inattentive; and (2) investors

update their beliefs in a na¨ıve Bayesian manner. Namely, some of the investors do not

observe the public signal, and all investors update their beliefs with respect to only their

own information, without taking into account the information sets and actions of others. In

particular, while all investors observe equilibrium prices in all periods, they do not use the

information contained in the price history to update their beliefs. These assumptions are

standard modeling devices in models of gradual information diffusion (see Hong and Stein

(1999), Hirshleifer and Teoh (2003), or Peng and Xiong (2006)).

I characterize the price path and trading volume following a news signal as a function

of the fraction of attentive investors F

t

(Section 4.1). The empirical predictions for the

differences in market dynamics following front page and non-front page news are then derived

in Section 4.2.

3.1 Evolution of Prices and Trading Volumes

I begin by characterizing the price levels and trading volumes in terms of the fraction

of attentive investors F

t

, without distinguishing whether the news signal is reported on the

front page or not.

Price levels. First, note that the uninformed investors hold the prior beliefs that the

return R is normally distributed with mean R and variance σ

2

R

. The informed investors

attend to the signal and update their beliefs in a na¨ıve Bayesian manner. Hence, their

beliefs are given by:

∀t ∈ {0, 1, 2, 3}, i ∈ I

t

: E

(i)

t

{R} =

σ

2

R + σ

2

R

N

σ

2

R

+ σ

2

; V ar

(i)

t

{R} =

σ

2

R

σ

2

σ

2

R

+ σ

2

(3)

Next, note that optimization of the mean-variance preferences given by (1) with the above

beliefs results in the following demand functions by the two groups of investors during any

13

period t:

∀t ∈ {0, 1, 2, 3}, i ∈ I

t

: x

(i)

t

=

σ

2

(R − P

t

) + σ

2

R

(N − P

t

)

σ

2

R

σ

2

(4)

∀t ∈ {0, 1, 2, 3}, i ∈ U

t

: x

(i)

t

=

R − P

t

σ

2

R

(5)

where P

t

denotes the price of the risky asset in period t.

The market clearing condition each period is that the total demand from the informed

and uninformed investors must equal the zero net supply. Hence, in each period t, the price

of the asset P

t

must satisfy:

∀t ∈ {0, 1, 2, 3} : F

t

σ

2

(R − P

t

) + σ

2

R

(N − P

t

)

σ

2

R

σ

2

+ (1 − F

t

)

R − P

t

σ

2

R

= 0 (6)

Solving this equation gives the following expression for the price of the asset during each

period t:

∀t ∈ {0, 1, 2, 3} : P

t

=

σ

2

σ

2

+ F

t

σ

2

R

R +

F

t

σ

2

R

σ

2

+ F

t

σ

2

R

N (7)

Absolute price changes. Taking the first differences yields the absolute price change

between any two consecutive periods:

∀t ∈ {1, 2, 3} : |∆P

t

| = |P

t

− P

t−1

| =

(F

t

− F

t−1

)σ

2

R

σ

2

|N − R|

(σ

2

+ F

t

σ

2

R

)(σ

2

+ F

t−1

σ

2

R

)

(8)

Price continuation. In order to calculate the continuation in the price path, recall that

the news signal has the form N = R + , where R and are independent normal variables

with R ∼ N (R, σ

2

R

) and ∼ N (0, σ

2

). Hence, price continuation, measured as the slope in

a regression predicting the price change in period t + 1 from the price change in period t, is

given by:

∀t ∈ {1, 2} : Cont(t, t + 1) =

Cov(∆P

t

, ∆P

t+1

)

V ar(∆P

t

)

=

F

t+1

− F

t

F

t

− F

t−1

σ

2

+ F

t−1

σ

2

R

σ

2

+ F

t+1

σ

2

R

(9)

Note that this expression is defined for any setting where a non-trivial set of investors

learns the news during the earlier period t. This holds for both the front page and the

non-front page news in my setting, since even in absence of reporting by the main source S,

news diffuses at the low but nonzero hazard rate ξ.

Trading volumes. Trading volume in each period t consists of all holdings that ex-

change hands between periods t − 1 and t. In each period, the newly informed investors, i.e.

investors i ∈ I

t

∩ U

t−1

change their demand following receipt of the news signal, inducing a

14

change in the equilibrium price and the other investors’ equilibrium holdings. Let x

(I)

t

de-

note the equilibrium holdings, in period t, of an investor i ∈ I

t

; similarly, let x

(U)

t

denote the

equilibrium holdings of an investor u ∈ U

t

. Trading volume in each period can be expressed

as a function of the newly informed investors’ holdings as follows:

∀t ∈ {1, 2, 3} : T V

t

= (F

t

− F

t−1

)|x

(I)

t

− x

(U)

t−1

| (10)

Taking the holdings from (4)-(5) and the equilibrium price levels from (7) then gives the

following expression for each period’s trading volume:

∀t ∈ {1, 2, 3} : T V

t

= (F

t

− F

t−1

)

(1 − F

t

)σ

2

+ F

t−1

(σ

2

+ σ

2

R

)

(σ

2

+ F

t

σ

2

R

)(σ

2

+ F

t−1

σ

2

R

)

|N − R| (11)

3.2 Empirical Predictions

I now compare the expressions for price changes, trading volumes, and price continuation

for front page and non-front page news, and derive empirical predictions for differential

market dynamics following different article positions.

Before proceeding, I note the evolution of the share of informed investors, F

t

, in the cases

of front page and non-front page news. In the first period, F

NF P

0

= F

F P

0

= 0. After that,

the share of informed investors following non-front page news evolves as follows:

F

NF P

t

=

γ for t = 1

γ + (1 − γ)ξ for t = 2

ξ + (1 − ξ)(γ + (1 − γ)ξ) for t = 3

(12)

Following front page news, meanwhile, the share of informed investors evolves as follows:

F

F P

t

=

γ for t = 1

γ + (1 − γ)γ for t = 2

ξ + (1 − ξ)(γ + (1 − γ)γ) for t = 3

(13)

Combining the shares of informed investors in (12)-(13) with the price changes in (8)

gives the immediate absolute price changes after non-front page and front page news:

|∆P

NF P

1

| =

γσ

2

R

σ

2

+ γσ

2

R

|N − R|; |∆P

F P

1

| =

γσ

2

R

σ

2

+ γσ

2

R

|N − R| (14)

Given that γ > γ, the first-period absolute price change is larger following front page

news than following non-front page news.

15

Similarly, trading volumes at the news release in the first period are given by:

T V

NF P

1

=

γ(1 − γ)

(σ

2

+ γσ

2

R

)

|N − R|; T V

F P

1

=

γ(1 − γ)

(σ

2

+ γσ

2

R

)

|N − R| (15)

The relationship between immediate trading volume around the news signal and the

percentage of immediately informed investors is non-monotonic. Trading volume is low if

either all or none of the investors see the news immediately, and trading volume is maximized

when the split between immediately attentive and inattentive investors is roughly even.

Recall that γ, << 1/2, reflecting the empirical setting I consider, where the proportion

of the population who see any news article immediately (within the first few minutes of

publication) is relatively low even for front page news. As a result, the split of attentive

versus inattentive investors is more equal and the immediate trading volume is higher when

the news is pinned to the front page.

Together, the price and volume expressions give the first empirical prediction regarding

the immediate market response to front page and non-front page news.

Prediction 1 (Immediate Market Response) Front page news articles are followed by

larger trading volumes and absolute price moves immediately (within minutes) after the news.

How does the price response play out outside of the immediate window? To see this, I

turn to the continuation in the price path. I begin with the short-term continuation:

Cont

NF P

(∆P

1

, ∆P

2

) =

(1 − γ)ξ

γ

×

σ

2

σ

2

+ [γ + (1 − γ)ξ]σ

2

R

(16)

Cont

F P

(∆P

1

, ∆P

2

) = (1 − γ) ×

σ

2

σ

2

+ [γ + (1 − γ)γ]σ

2

R

(17)

Note that from condition (2), the first term of Cont

F P

(∆P

1

, ∆P

2

) is larger than the

first term of Cont

NF P

(∆P

1

, ∆P

2

). The second term is larger in Cont

NF P

(∆P

1

, ∆P

2

), since

γ > γ > ξ. However, for sufficiently low levels of immediate attention γ and γ, the former

effect dominates. This results in the following empirical prediction.

Prediction 2 (Immediate Return Continuation) Front page news articles are accom-

panied by higher continuation in the short-term price changes.

While front page news articles are followed by a larger immediate reaction that continues

in the short-term, the longer term dynamics are quite different. To see this, note that the

continuation in returns from the second to the third period for front page and non-front page

news is given by:

16

Cont

NF P

(∆P

2

, ∆P

3

) = (1 − ξ) ×

σ

2

+ γσ

2

R

σ

2

+ [ξ + (1 − ξ)(γ + (1 − γ)ξ)]σ

2

R

(18)

Cont

F P

(∆P

2

, ∆P

3

) =

(1 − γ)ξ

γ

×

σ

2

+ γσ

2

R

σ

2

+ [ξ + (1 − ξ)(γ + (1 − γ)γ)]σ

2

R

(19)

Note that with ξ < γ < γ << 1/2, expressions (18)-(19) imply that the continuation from

the second period to the third is actually lower for front page news compared to non-front

page news. This yields the third empirical prediction of the gradual information diffusion

framework.

Prediction 3 (Delayed Return Continuation) Front page news articles induce lower

continuation in the long-term price changes.

In the next section, I test Predictions 1, 2, and 3 by observing the market dynamics

following front page and non-front page Bloomberg news articles in my hand-collected sam-

ple. For the immediate news release window, t = 1, I look at the 5-10 minutes following

publication of each individual news article. As the short-term subsequent window, t = 2, I

consider 30-45 minutes following the news, as the front page news articles tend to remain

prominently positioned for approximately half an hour to an hour. For the longer horizon,

t = 3, I consider windows of 60, 90, and 120 minutes following the news release.

4 News Positioning and Market Dynamics

Using the natural experiment in news positioning, in this section, I empirically estimate

the causal effect of front page news positioning on financial markets.

4.1 News Positioning and Short-Term Market Dynamics

I begin the analysis of differential activity following comparable front page and non-front

page news articles by observing the short-term trading volume surges and price dynamics

following the two types of SI news. Placing a piece of news on the front page is associ-

ated with substantially larger trading volumes and absolute price changes within minutes of

publication, as well as with higher continuation in the short-term price paths.

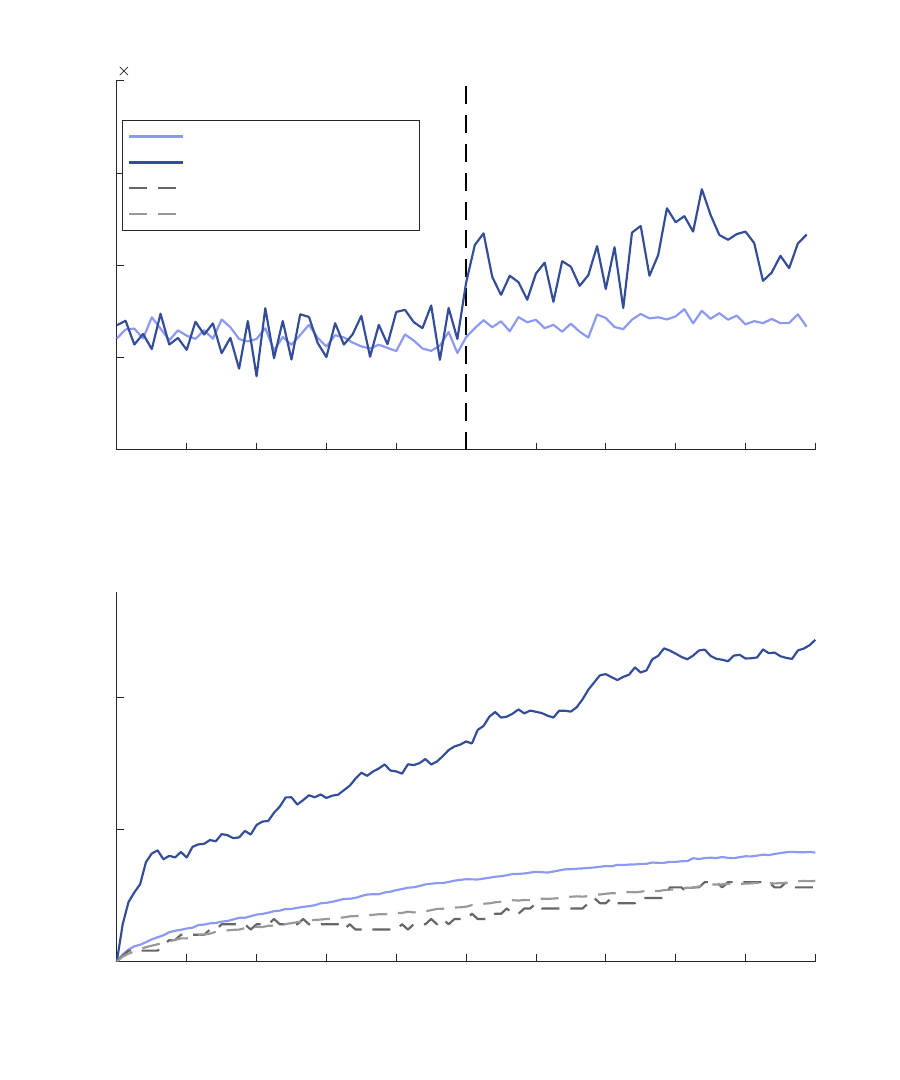

Consistent with Prediction 1, the more saliently positioned front page news articles induce

significantly higher trading volumes. The median 15-second trading volume, computed as

the percentage of shares turned over during the ten minutes before and after SI news articles,

is displayed in Panel 1 of Figure 5. The median non-front page SI news article is accompanied

17

by virtually no increase in trading volume (plotted in light blue in the figure) relative to the

pre-news baseline. There is, however, a pronounced increase in the trading volumes following

SI news articles that appear on the front page (displayed in dark blue). The difference in

averages is even starker. Over the ten minutes after a news release, the average non-front

page SI news article is accompanied by a total of 0.05% turnover. The average ten-minute

trading volume after front page news is almost four-fold larger, at 0.19%. The difference is

statistically significant at the 1% level, with a t-statistic of 4.52, as reported in Panel 1 of

Table 3. The estimated difference remains identical when controlling for month and hour

fixed effects, log market capitalization, and industry fixed effects.

Does the increased market activity reflected in trading volume correspond to larger price

changes? Panel 2 of Figure 5 presents the average absolute percentage price changes following

front page and non-front page SI news articles. The absolute price changes are calculated

separately for each firm over every five-second interval. The graph averages the price changes

in event time over the cross-section of firms. As a reference, the graph also plots, in dashed

lines, the baseline price changes computed over the same time period for the same securities

24 hour prior to the publication of the news articles. Confirming the comparability of the two

sets of articles, the pre-news baselines are statistically indistinguishable for the two samples

of news articles. After publication, both front page news articles and non-front page news

articles are accompanied by larger absolute price changes than their respective baselines.

Two patterns emerge from a visual inspection of the absolute price changes. First, the

overall price change from the time of news publication to ten minutes later is much larger for

SI news articles that are positioned on the front page than for those that are not. Second,

corresponding to the more persistent attention garnered by the front page news articles being

saliently positioned for longer, price changes after these news articles are more persistent. I

consider these two effects in greater detail below.

I begin the statistical analysis of price effects by looking at the differential immediate

price reactions to front page and non-front page SI news articles. Lending further support to

Prediction 1, the average absolute price change within the first ten minutes after front page

SI news articles is 60 basis points, compared to 21 basis points for non-front page SI news.

The difference of 39 basis points is statistically significant at the 1% level, with a t-statistic

of 5.91, as can be seen from Panel 2 of Table 3. The result is robust to the inclusion of

controls: the estimated difference is 40 basis points when accounting for month and hour

fixed effects, and 36 basis points when also controlling for log market capitalization and

industry fixed effects. The results are similar at a shorter horizon of five minutes following

the news, with an average absolute price change of 42 basis points accompanying front page

news articles, compared to 16 basis points for non-front page news articles (t-statistic on

18

the difference is 6.19). The contrast is less stark, but still significant when the window is

extended to one hour following the news. The average absolute price change over the hour

following front page SI news articles is 0.98%, whereas the average absolute price change

over the hour following non-front page SI news articles is 0.51% (t-statistic on the difference

is 5.01).

Having established empirical support for the first prediction of my conceptual framework,

I now turn to Prediction 2. The theoretical prediction states that price paths following the

front page SI news articles should display more short-term continuation, reflecting the more

persistent attention garnered by news articles that stay at the top of the terminal screen for

longer. I test the extent to which front page positioning induces higher short-term return

continuation formally by estimating the following specification:

Ret

s,i,[t+t

1

,t+t

2

]

= α + β

1

Ret

s,i,[t,t+t

1

]

+ β

2

F P

s

+ β

3

Ret

s,i,[t,t+t

1

]

× F P

s

(20)

+γX

i,t

+

s,i,[t+t

1

,t+t

2

]

,

where Ret

s,i,[t,t+t

1

]

denotes the return on security i during the immediate period [t, t + t

1

]

after publication of news article s, and Ret

s,i,[t+t

1

,t+t

2

]

is the return during the delayed period

[t+t

1

, t+ t

2

]. F P

s

is an indicator variable equal to one for SI news articles that are pinned to

the front page and zero for SI news articles not on the front page. The controls X

i,t

include

month and hour of day fixed effects, as well as log firm size and industry fixed effects. The

tests are run over the following time windows: (t

1

, t

2

) ∈ {(3 min, 5 min), (5 min, 10 min),

(5 min, 15 min), (5 min, 20 min), (10 min, 20 min), (10 min, 30 min)}.

Confirming Prediction 2, front page news articles are followed by higher serial correlation

in returns at all considered short-term horizons, except for the shortest horizon of (t

1

, t

2

) =

(3 min, 5 min). The coefficient of interest, β

3

, is positive and statistically significant across

the other time specifications, as displayed in Table 4. For example, relative to non-front page

SI news articles, front page SI news articles induce 17% more continuation in returns from

the first five minutes after publication to the next five minutes. This result is economically

sizable. For every 1% price move within the first five minutes after a front page SI news

articles, there is an additional 17 basis points move in the same direction during the following

5 minutes, compared to non-front page SI news articles. The effect is also precisely estimated,

with a t-statistic of 5.70 without controls, 5.67 with month and hour fixed effects, and 5.57

with the full set of controls including log firm size and industry fixed effects. Results over

other windows are qualitatively similar, with the coefficient β

3

falling between 0.17 and 0.32,

depending on the considered time windows.

Interestingly, the non-front page SI news articles are actually followed by short-term re-

19

turn reversal from the first five minutes to the next five to ten minutes, consistent with

the literature on short-term price reversals.

6

The coefficient on Ret

s,i,[t,t+t

1

]

not inter-

acted with the front page indicator is negative and statistically significant for (t

1

, t

2

) ∈

{(5 min, 10 min), (5 min, 15 min), (5 min, 10 min)}. Effectively, these news articles, which

are prominently positioned at the top of the terminal screen only for short periods of time,

see the initial five-minute price reactions partially reverse within the following minutes. On

the other hand, front page SI news articles, which are prominently positioned for longer, are

followed by a strong price drift over the short term.

4.2 News Positioning and Longer-Term Price Dynamics

Placing a piece of news on the front page induces sizable short-term price effects; do we

see the non-front page information eventually catch up? As the front page news articles get

removed from their prominent positions, the differences in diffusion of information contained

in these articles and the non-front page articles gradually diminish. The conceptual frame-

work predicts that at longer horizons, front page news articles should see less continuation

in returns. I find evidence in support of this prediction: over longer horizons of one to two

hours after the news, non-front page information induces substantially more price drift than

front page news. The incorporation of non-front page information is much slower, however,

and full convergence does not occur for days after the news.

I begin evaluating longer-term price continuation by estimating specification (20) over

the following windows: t

1

∈ {5 min, 10 min} and t

2

∈ {45 min, 60 min, 90 min}. The results

are reported in Panel 1 of Table 5.

The results reveal an interesting pattern of dynamics: the immediate returns over the

first five minutes after news publication are more positively predictive of subsequent returns

following front page news than following non-front page news, up to approximately forty-

five minutes. But over longer horizons of sixty or ninety minutes, the effect is no longer

present. Continuation in returns from the first five minutes to the remainder of the first

hour is statistically indistinguishable for front page versus non-front page SI news articles.

From the first five minutes to the remainder of the first hour and a half, there is slightly less

continuation following front page news (significant at the 10% level).

Similarly, the initial ten-minute returns induced by front page news are followed by a

stronger drift for about forty-five minutes. During the first forty-five minutes, front page

news articles induce an additional drift of approximately 31% of the initial ten-minute return.

6

See, for example, Atkins and Dyl (1990), Ederington and Lee (1995), Fung, Mok, and Lam (2000),

Chordia, Roll, and Subrahmanyam (2002), Zawadowski, Andor, and Kert´esz (2006), and Heston, Korajczyk,

and Sadka (2010).

20

Expanding the window to sixty minutes, the continuation becomes statistically indistinguish-

able between front page and non-front page news, and at ninety minutes there is weakly more

continuation for article that are not pinned to the front page.

As I shift the window even further, the results lend empirical support to Prediction 3.

Panel 2 of Table 5 reports estimates of specification (20) over the following windows: t

1

∈

{30min, 45min} and t

2

∈ {90min, 120min}. The non-front page news articles are followed,

on average, by 25-27% continuation in returns from the first half-hour to the remainder of

the 90-120 minutes. Front page news articles, however, see 14-19% less continuation. The

differences are highly statistically significant. Similarly, the returns from the first forty-five

minutes are substantially less likely to continue if the news article is pinned to the front

page. Non-front page news articles see a continuation of 19-22% from the first 45 minutes

to the remainder of the first 90-120 minutes. By contrast, front page news articles actually

see no return continuation over the same time windows.

Coupled with the results in Table 4, the longer-term price dynamics highlight the differ-

ences in the speed of incorporation of front page and non-front page information. Pinning a

piece of news on the front page induces a stronger drift in returns up to forty-five minutes,

and the reactions to non-front page articles begin to catch up over the remainder of the

first couple of hours after news publication. Theoretically, these patterns are fully consis-

tent with the gradual information diffusion framework outlined in Section 3. Practically,

the results indicate that for news articles consumed by sophisticated finance professionals

through a subscription-based platform such as Bloomberg, the market dynamics track the

discretionary positioning in real time.

While the price impact of front page information occurs quickly, it takes substantially

longer for non-front page information to be fully reflected in asset prices. Table 6 presents

the average differences in trading volumes and absolute price changes one, two, five, ten,

and fifteen days after front page and non-front page SI news articles. The differences are

estimated controlling for month and hour fixed effects, log market capitalization, and indus-

try fixed effects. For the trading volume tests, I look at the total trading volume over a

10-minute window d days after news publication, where d ∈ {1, 2, 5, 10, 15}. Similarly, the

absolute price changes are calculated as the absolute percentage difference in price from the

time of news publication to exactly d days later.

The results indicate that some of the non-front page information is reflected in prices

within the first few days, but a portion of the gap in market reactions induced by positioning

remains even days after the news. The elevated level of trading volume accompanying front

page news lasts for at most two days (the difference is statistically significant at the 1% level

one day out, and at the 10% level two days out). The difference in absolute price changes one

21

day after the news is highly statistically significant, but milder than the difference from just

the first hour, tabulated in Table 3. This difference declines slightly but remains economically

similar two days after the news, significant at the 5% level. Five days after news publication,

the price impact of front page positioning declines substantially and is no longer statistically

significantly different from the price impact of non-front page news, although the difference

remains economically visible at around 25 basis points. The gap is milder still, at 18 basis

points, ten days out after the news, and converges to a statistically indiscernible 8 basis

points fifteen days out after the news.

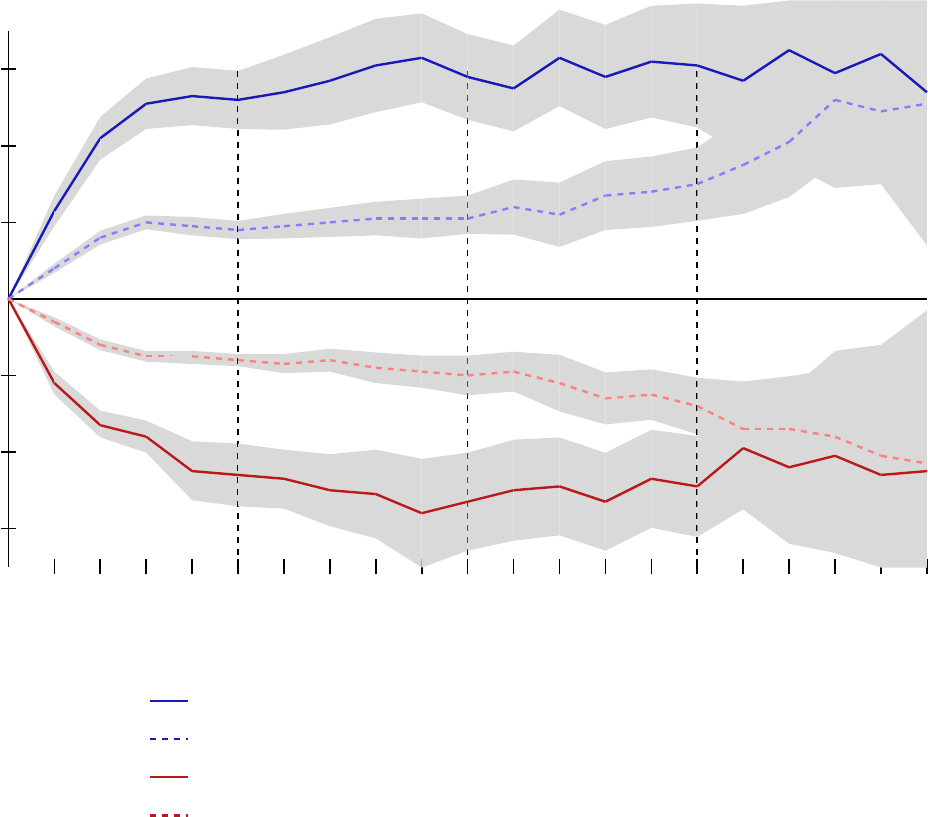

These patterns are reinforced in a graphical evaluation of the directional price paths

following front page and non-front page news, displayed in Figure 6. I group the SI news

articles in my sample along two dimensions: (1) their position (front page versus non-front

page) and (2) the direction of the initial five-minute price move (positive versus negative). I

take the average cumulative price paths across news articles in each category, in event time

from the time of publication to various time windows. These price paths are plotted in solid

lines for front page news and in dashed lines for non-front page news. The price paths for

articles accompanied by positive initial five-minute price changes are shown in blue, while

the price paths for articles accompanied by negative initial price changes are shown in red.

In each case, the price change accompanying a given piece of news is computed relative to

the market return over the same time period, in order to screen out the directional equity

premia at longer horizons. Standard error bars are shaded in gray.

The figure shows a variety of time windows ranging from minutes to days after the news.

In the immediate term (0-10 minutes, displayed in the first quarter of the figure), front page

news articles are accompanied by larger price changes, in both the positive and the negative

domains, consistent with the absolute price change results reported in Panel 2 of Table 3.

This gap widens for about 45 minutes, and then begins to narrow, as can be seen from the

price paths over the first hour after news publication. The narrowing of the gap continues

for hours after the news, as front page articles see no additional price moves, while non-front

page information continues being incorporated into prices. In the last quarter of the figure,

I show the price responses from publication to one, two, five, ten, and fifteen days out after

the news. Although the standard errors become very wide at these horizons, the economic

magnitudes show no difference in the long-term reactions to front page versus non-front

page news, due to the non-front page news articles gradually catching up to their front page

counterparts.

Overall, the effect of differential news positioning is stark and quick, and takes a while to

converge. The gradual catching up of the reactions to non-front page information begins as

early as an hour after publication, but the diffusion of information in non-front page news

22

is quite slow. As a result, the effect of news positioning can be statistically noticeable and

economically meaningful even several days after the news.

5 News Positioning versus News Importance

In this section, I compare the estimated effects of news positioning against the effects

of news importance, as marked by the editorial staff. I estimate the relationship between

news importance and market dynamics by concentrating on news articles that are all equally

prominently positioned but that vary in importance – i.e., by comparing front page news

articles from the PI and SI categories. The difference in market reactions following these two

types of news is qualitatively different from and quantitatively weaker than the difference

induced by front page positioning.

I limit my attention only to news articles that are pinned to the front page, so that there is

no variation in the prominence of the article positions. I include all front page news articles,

regardless of their importance markings, and estimate the difference in market reactions

following the more (“primary important”) and less important (“secondary important”) news

articles.

First, I note that the trading volumes immediately following front page PI news articles

are not statistically different from the trading volumes following front page SI news articles.

As displayed in Panel 1 of Table 7, during the first five minutes after a front page news article,

on average, an additional 0.09% of shares turn over when the article is from the PI category,

but this difference is not statistically significant. Similarly, during the first ten minutes, front

page PI news articles are followed by an additional 0.10% in trading volume compared to

front page SI news articles, significant only at the 10% level. The pattern remains similar

over longer horizons, with an average of 0.18% additional shares turned over during the hour

following front page PI news articles, with the difference remaining statistically insignificant.

Second, while PI articles are accompanied by larger price impact than SI articles, the

effect is less significant and less persistent than the difference in absolute price changes

induced by front page positioning. As can be seen from Panel 2 of Table 7, in the first

five minutes, front page PI news articles are followed by an additional 0.35% absolute price

change, an increase of 80% over the front page SI articles; the difference is significant but

statistically weaker than the difference between front page and non-front page SI articles.

The difference in absolute price changes following front page PI news articles versus front

page SI news articles remains similar in magnitude and declines in statistical significance as

the window is extended to ten and then sixty minutes. Overall, PI news articles are followed

by larger price reactions immediately in the first five to ten minutes, but do not see further

23

differences from the front page SI news articles over longer horizons. This contrasts with the

difference between front page and non-front page SI news articles documented in Table 3,

which continues to grow over the hour following the news.

This result is corroborated by a comparison of the continuation in the price paths follow-

ing PI and front page SI news articles, which I estimate using the following specification:

Ret

s,i,[t+t

1

,t+t

2

]

= α + β

1

Ret

s,i,[t,t+t

1

]

+ β

2

P I

s

+ β

3

Ret

s,i,[t,t+t

1

]

× P I

s

(21)

+γX

i,t

+

s,i,[t+t

1

,t+t

2

]

,

where Ret

s,i,[t,t+t

1

]

denotes the return on security i during the immediate period [t, t + t

1

]

after publication of news article s, and Ret

s,i,[t+t

1

,t+t

2

]

is the return during the delayed period

[t + t

1

, t + t

2

]. P I

s

is an indicator variable equal to one if the front page article comes from

the “primary important” category and zero if the article is from the “secondary important”

category. The controls X

i,t

include month and hour fixed effects, log firm size, and industry

fixed effects. The considered time windows are (t

1

, t

2

) ∈ {(5 min, 10 min), (5 min, 15 min)}.

Table 8 presents the results.

The estimated coefficient on Ret

s,i,[t,t+t

1

]

× P I

s

indicates that front page PI news articles

are not accompanied by any more short-term price drift compared to front page SI news

articles. The difference is neither economically notable, nor statistically significant. Over

the same time horizons, the difference in price drift following front page and non-front page

SI news articles is 17% and highly statistically significant (see Table 4).

Recall that this analysis considers only news articles positioned on the front page, but of

both categories: “primary important” and “secondary important.” Whereas the results in

Section 4.2 keep article importance constant (only SI articles) and vary front page position-

ing, the analyses in this section keep the positioning constant but vary article importance.

As can be seen from a comparison of Tables 7-8 against Tables 3-4, differences in article

importance correspond to milder differences in market dynamics than differences in article

positioning. These findings suggest that article positioning is even more instrumental in

driving market reactions than differences in article importance, as marked by Bloomberg’s

journalistic and editorial staff and confirmed by the target audience of finance professionals

(see Section 6.3 below).

5.1 Discussion: Attention versus Inference

The comparison of differential reactions to news position and news importance helps

highlight the channel behind the market response to front page positioning. The drift patters

24

associated with prominent positioning, which are not observed for differential importance,

indicate that the positioning effect is driven by attention patterns rather than inference

regarding the importance of the underlying news.

Effectively, there are two mechanisms that could induce heightened market activity fol-

lowing front page news articles relative to non-front page articles. First is the attention

channel highlighted by the conceptual framework in Section 3: front page news articles re-

ceive more immediate attention, corresponding to higher trading volumes and absolute price

changes. The second mechanism is inference regarding the importance of the underlying

news: investors perceive the superior position to signal greater importance of the front page

articles.

While both channels produce increases in immediate trading volumes and price changes,

only the attention channel predicts the type of subsequent dynamics observed in the data.

As captured by Predictions 2 and 3, the attention channel predicts that front page articles

should be accompanied by more short-term drift and less continuation at longer horizons.

If instead the initial reactions are driven by inference regarding the articles’ importance,

there is no reason to observe a pattern of higher short-term drift and subsequent gradual

convergence.

The results on the differences between PI and SI front page news articles further support

the gradual information diffusion interpretation. The differences between reactions to articles

of actual varying importance are immediate, inducing no differential drifts. If the effect of

positioning were driven primarily by the inference channel, then the timing of the positioning

effect should be comparable to the effect of importance. Instead, differential positioning

induces differences in incorporation of information that creates predictability in returns at a

variety of horizons. This corresponds more closely to the timing of the conceptual model of

gradual information diffusion.

Altogether, the effects of news positioning are not only more substantial than the dif-

ferences between articles of varying editorial importance in the immediate term, but also

induce differences in return predictability further out. These results support the importance